Downsizing Seniors in Fulton County: Deed in Lieu vs Short Sale

Tax Pitfalls, Credit Impact, and What to Do First

You’ve owned your Fulton County home for 30 years. The mortgage is underwater, the property taxes are climbing, and you’re ready to downsize — but you’re not sure whether a deed in lieu or a short sale is the right exit. Choose the wrong one, and you could face an unexpected tax bill, a damaged credit score, or both. And in retirement, those consequences follow you a lot longer than they would at 40.

Deed in lieu vs short sale is one of the most consequential decisions a senior homeowner can make, yet most people approach it without fully understanding the differences. Both options allow you to exit an unaffordable or underwater mortgage without going through a full foreclosure — but they work differently, carry different lender requirements, affect your credit differently, and most importantly, create very different tax outcomes.

Fulton County’s rapidly rising property values create a unique dynamic for seniors. Some are equity-rich but cash-poor, squeezed by a mortgage taken during a refinance years ago. Others are genuinely underwater. The right option depends on which situation you’re actually in — and knowing that starts with understanding both paths clearly.

In this guide, we’ll walk through exactly what each option involves, how they compare side by side, what the tax pitfalls are that most seniors never see coming, and how to determine which path makes the most sense for your specific situation.

What Is a Deed in Lieu of Foreclosure? (And Who It’s For)

A deed in lieu of foreclosure is an arrangement where you voluntarily transfer the title of your home directly to your mortgage lender in exchange for being released from your mortgage obligation. There is no court process, no auction, no public foreclosure proceeding — you simply sign over the deed, and in exchange, the lender agrees to release you from the debt.

Lenders sometimes prefer a deed in lieu because it is faster and cheaper than going through foreclosure. For seniors who want a clean, relatively quick exit from a home they can no longer afford or maintain, a deed in lieu can feel like the emotionally simpler option. There’s one transaction, one conversation with the lender, and a defined end date.

What Lenders Typically Require

• The home must usually be listed for sale for a minimum period first — often 90 days — as proof that a traditional sale was attempted

• There can be no junior liens on the property: no second mortgage, no home equity line of credit, no HOA lien, no IRS tax lien. A single unresolved lien can disqualify you entirely

• You must demonstrate genuine financial hardship through documentation

• The property must be in reasonable condition

• The lender must agree — a deed in lieu is not a right you can invoke unilaterally; it is a negotiated outcome

What Seniors Get in Exchange

In a deed in lieu, you typically receive a release from the deficiency balance — the gap between what the home is worth and what you still owe. Some lenders also offer relocation assistance, sometimes called “cash for keys,” to encourage a smooth and timely vacating of the property. What you give up is the property itself, any remaining equity, and control over the sale price or timeline.

One Georgia-specific note worth knowing: Georgia is a non-judicial foreclosure state, which means lenders can move through the foreclosure process in as little as 37 days from notice to sale. That speed actually gives seniors negotiating leverage — a lender who knows foreclosure is fast may still prefer the cleaner, more cooperative deed in lieu process. Understanding how mortgage servicers handle these requests is important, and the CFPB’s guide to mortgage servicer obligations is a useful starting point for knowing your rights in that conversation.

What Is a Short Sale? (And How It Works in Fulton County)

A short sale is when you sell your home for less than the outstanding mortgage balance, with your lender’s prior approval, and the lender agrees to accept the sale proceeds as full — or at least partial — satisfaction of the debt. The word “short” refers to the sale proceeds falling short of what’s owed, not to the timeline.

The Short Sale Process Step by Step

• You list the home for sale, typically working with a real estate agent experienced in short sale transactions

• A buyer makes an offer

• You submit the offer to your lender along with a hardship package — a letter explaining your financial situation, income documentation, and asset information

• The lender reviews and approves, rejects, or counters the offer — this review process is what makes short sales slow

• Once approved, the sale closes and the lender receives the proceeds

Timeline and Fulton County Realities

A short sale typically takes three to six months from listing to closing. For seniors, that extended timeline carries real costs: continued property tax accrual, ongoing maintenance obligations, HOA fees, utility bills, and the emotional weight of a prolonged process with an uncertain outcome.

Fulton County’s strong seller’s market creates a specific challenge: in neighborhoods where homes are selling at or near full value, lenders may push back on short sale approvals because they believe the property can sell for more. Seniors in high-demand areas like Cascade Heights, College Park, or Adamsville may find it harder to get a short sale approved than those in softer markets.

The Deficiency Question

This is the most critical point in any short sale negotiation: lenders may or may not agree to waive the deficiency balance. If your home sells for $180,000 and you owe $240,000, the $60,000 gap is the deficiency. Whether the lender forgives that amount or pursues collection must be negotiated explicitly and confirmed in writing — in the short sale approval letter — before closing. Never assume a short sale eliminates the deficiency unless you have it in writing.

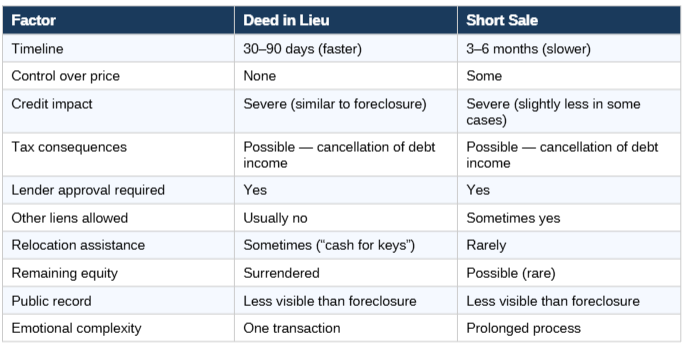

Deed in Lieu vs Short Sale — Side-by-Side Comparison

Here’s how the two options compare across the factors that matter most to senior homeowners in Fulton County. Use this as a starting framework, then read the detail beneath the table before drawing any conclusions.

Looking at this table, the deed in lieu appears faster and simpler — and it often is. But the critical variable is lien status. If your Fulton County property carries a second mortgage, an outstanding home equity line, an HOA lien, or any IRS-related encumbrance, a deed in lieu may simply not be available to you. A short sale, which allows more time and flexibility to negotiate existing liens, may be your only real option.

The other variable most seniors underestimate is the tax consequence. Both options can trigger a significant and unexpected tax event the following January. That consideration — which we cover in detail in the next section — should drive the decision as much as any other factor.

The Tax Pitfall Most Seniors Don’t See Coming

This is the section most homeowners wish they had read before signing anything.

When a lender forgives or cancels a debt — including the deficiency balance in either a deed in lieu or a short sale — the IRS may treat that forgiven amount as taxable income. This is called cancellation of debt income, or COD income, and it is one of the most misunderstood aspects of both transactions.

How It Works in Practice

If you owe $250,000 on your Fulton County home, the property transfers or sells for $180,000, and the lender forgives the $70,000 difference — you may owe income tax on that $70,000 as if it were wages earned that year. The lender reports this to the IRS using a 1099-C (Cancellation of Debt) form, which you will receive the following January. Many seniors exit their homes with no cash proceeds and are then blindsided by a tax bill months later.

Key Exemptions Seniors Should Know Before Signing

• Mortgage Forgiveness Debt Relief Act: This provision has historically allowed homeowners to exclude forgiven debt on a primary residence from taxable income. It has been extended multiple times by Congress. Verify the current status with a licensed CPA before your transaction closes — do not rely on what was true in a prior year.

• Insolvency Exemption (IRS Form 982): If your total liabilities exceeded your total assets immediately before the debt cancellation, you may qualify to exclude some or all of the COD income from your taxable income. For seniors on fixed incomes with limited assets, this exemption is frequently applicable and frequently overlooked. The

• Bankruptcy Exclusion: If the debt was discharged through bankruptcy proceedings, it is excluded from taxable income entirely.

Georgia State Tax Treatment

Georgia generally conforms to federal tax treatment on cancellation of debt income, but the specifics depend on which federal provisions are currently in effect and whether Georgia has adopted them. Always verify with a Georgia-licensed CPA or enrolled agent before closing — not after.

Critical: Before signing any deed in lieu or short sale agreement, consult a tax professional and a HUD-approved housing counselor. The tax event triggered by either transaction can exceed what you expected to “save” by avoiding foreclosure. This is not a step to skip.

Credit Score Impact — What Seniors Should Actually Expect

Let’s be direct: both a deed in lieu and a short sale will significantly damage your credit score. This is not a scare tactic — it’s the reality that allows you to plan around it rather than be surprised by it.

How Each Transaction Is Reported

A deed in lieu is typically reported to the credit bureaus as “deed in lieu of foreclosure” or “settled for less than full balance.” FICO scoring models treat this very similarly to an actual foreclosure. A short sale is usually reported as “settled for less than full balance” — and while some lenders report it more favorably, many do not. The difference between the two in credit impact is often smaller than homeowners hope.

Both events typically cause a score drop of 85 to 160 points depending on your starting score and other factors on your report. Both remain on your credit report for seven years. The practical score impact does diminish over time, particularly if you avoid adding new negative items after the transaction.

For a thorough explanation of how these events are reported and what your rights are throughout that process, the CFPB’s mortgage key terms and credit guidance is a reliable and authoritative resource.

Why Credit Impact Matters Differently for Seniors

• If you’re downsizing to rent, landlords in competitive Atlanta-area markets — particularly in Buckhead, Midtown, and Sandy Springs — run credit checks. A recent deed in lieu or short sale can make securing quality housing significantly harder

• If you need to co-sign for a family member or access any credit-based financial product in retirement, damaged credit limits those options

• Future mortgage eligibility: FHA guidelines typically require a 3-year waiting period after both a deed in lieu and a short sale (with limited exceptions). Fannie Mae guidelines differ and may allow re-entry sooner under specific circumstances

The Silver Lining

For seniors who are genuinely transitioning to renting, assisted living, or moving in with family — and who have already secured that next housing situation — the credit impact may matter less than it feels in the moment. The question is not only what happens to your credit, but how much your future financial life actually depends on it.

Lender Requirements and the Hidden Obstacles Seniors Face

Both a deed in lieu and a short sale require the lender’s active cooperation and approval. Neither is a right you can exercise unilaterally. And both come with documentation requirements and eligibility criteria that create real obstacles — particularly for senior homeowners who have accumulated liens or have loans that have been sold to secondary market investors.

Common Lender Requirements for Deed in Lieu

• Proof that the property was actively listed for sale for a minimum period (typically 90 days) with no acceptable offers

• No junior liens, second mortgages, home equity lines, HOA liens, contractor liens, or IRS encumbrances on the title — any one of these typically disqualifies the deed in lieu

• A documented hardship letter with supporting financial statements

• Property must be in reasonable condition and not subject to city code violations that would prevent transfer

Common Lender Requirements for Short Sale

• A detailed hardship letter explaining why you cannot continue making mortgage payments

• Proof of income and assets so the lender can assess whether you genuinely lack the ability to make up the deficiency

• Clear title at closing — existing liens typically must be negotiated down or paid

• An arm’s length transaction — the buyer cannot be a family member or anyone with a prior relationship to the seller

The Lien Problem for Long-Term Fulton County Homeowners

Many seniors who have owned their Fulton County homes for 20 or 30 years have accumulated layers of financial encumbrances they may not even be fully aware of: a home equity line of credit from a renovation, unpaid HOA dues from a period of hardship, a contractor lien from a disputed repair, or an IRS tax lien from a prior year’s delinquency. Any of these can derail a deed in lieu entirely and seriously complicate a short sale.

If delinquent property taxes are also part of the picture, those must be resolved at or before closing in either scenario. They will not simply go away because the home transfers to a new owner or lender.

The Servicer vs. Investor Distinction

If your loan has been sold to investors through securitization — common with mortgages originated in the 2000s and 2010s — the company currently collecting your payments (the servicer) may not have authority to approve a deed in lieu or short sale without investor consent. This can add months to what you expected to be a simple process. Ask your servicer early whether investor approval is required.

Which Option Is Right for You? A Framework for Fulton County Seniors

Every homeowner’s situation is different. The right choice between deed in lieu and short sale depends on your lien situation, your lender’s willingness to cooperate, your tax exposure, how quickly you need to exit, and what your next housing situation will look like. Here’s a practical framework.

Choose a Deed in Lieu If:

• You have only one mortgage and no other liens on the property

• Your lender has indicated willingness to consider it

• You need to exit within the next 30 to 90 days and cannot afford a prolonged process

• You don’t need to retain any control over the sale price or the buyer

Choose a Short Sale If:

• You have multiple liens that can be negotiated during the sale process

• You want some control over who buys the property and at what price

• Your lender is more likely to approve a sale than a voluntary deed transfer

• You have more time to work through a 3-to-6-month process without the property reaching foreclosure

Consider Neither If:

You have significant equity. In Fulton County’s market, some seniors who believe they are underwater are actually not — they simply haven’t had the home recently valued. A proper appraisal or broker’s price opinion may reveal equity that makes a traditional sale — or even an as-is cash sale — the right move. Selling at market value generates real proceeds that pay off the mortgage and put money in your pocket. Do not choose a deed in lieu or short sale if you have equity you haven’t accounted for.

Get Professional Guidance First If:

You have an IRS lien, delinquent property taxes, an HOA dispute, or any uncertainty about your tax exposure. These variables change the math entirely. The HUD-approved housing counselor locator connects you with free or low-cost professional advisors who can help you understand exactly where you stand before you make an irreversible decision. HUD counselors are available in the Atlanta metro area and can walk through your full financial picture with you confidentially.

The biggest mistake seniors make in this situation is choosing between these two options without first determining whether they need either one. Before you sign anything, talk to someone who can review your specific situation — your lien status, your equity position, your tax exposure, and your timeline.

Final Thoughts: The Right Exit Is the One That Protects Your Retirement

Deed in lieu vs short sale is not a simple choice, and it’s not one you should make based on what a neighbor did or what you read in a single article. Both options carry real consequences — credit damage that follows you for seven years, potential tax bills that arrive the following January, and lender requirements that may not match your actual situation.

What matters most is that you understand both options clearly, verify your equity position before assuming you’re underwater, and talk to a tax professional and a housing counselor before signing anything. For senior homeowners in Fulton County, this decision intersects with retirement income, Social Security, future rental eligibility, and long-term financial health in ways that make getting it right especially important.

Not Sure Which Option Fits Your Situation? Let’s Talk.

If you’re a senior homeowner in Fulton County weighing a deed in lieu vs short sale — or simply trying to understand your options before making a decision that can’t be undone — reach out to Atlanta Housing 411 today. I’m Gerald Harris, and I work with homeowners across Atlanta and Fulton County who are navigating exactly this kind of transition. Before you sign anything, let’s talk through your specific situation. The right option for your neighbor may be the wrong option for you.

📞 Call or Text: 404-913-7086 📧 Email: atlanta285.com@gmail.com

Visit Atlanta Housing 411 — Contact Gerald Harris — No pressure. No judgment. Just honest local guidance.