How to Stop Foreclosure in Georgia Before the Courthouse Steps

A Fulton County Homeowner’s Guide

In Georgia, a lender can take your home from the first missed payment notice to the courthouse steps auction in as little as 37 days. No lawsuit. No judge. No second chance once the gavel falls.

That is not an exaggeration. Georgia is a non-judicial foreclosure state, which means your lender does not need to go to court to foreclose on your home. The entire process — from notice to sale — happens outside the legal system, faster than most homeowners realize is even possible. By the time many Atlanta-area homeowners understand what’s happening, the window to act is already narrow.

Missing mortgage payments does not make someone a bad homeowner. Job loss, a medical crisis, divorce, and rising property taxes are the most common triggers for foreclosure among Fulton County homeowners — situations that can happen to anyone. What matters is understanding your options and acting on them before a courthouse steps sale makes the decision for you.

Here is what many Atlanta homeowners don’t realize: in today’s Fulton County market, a home worth $280,000 with a $200,000 mortgage balance is not a hopeless situation. It is an asset with $80,000 in equity that can be protected — if you act before the sale date. This guide will walk you through all five options to stop foreclosure in Georgia, what each one involves, and how to choose the right path for your specific situation.

Why Georgia’s Foreclosure Timeline Is Unlike Any Other State

Before we discuss how to stop foreclosure in Georgia, you need to understand exactly why the timeline is so unforgiving — and why acting today, not next week, is the difference between having options and having none.

Georgia is a non-judicial foreclosure state. That single fact changes everything. In states like Florida or New York, a lender must file a lawsuit to foreclose, giving homeowners months or even years to respond, negotiate, or appeal. In Georgia, the lender handles the entire process privately, through notice and advertisement, with no court involvement required.

Georgia’s Foreclosure Timeline Step by Step

• Day 1: A mortgage payment is missed. Most loans include a 15-day grace period before a late fee is assessed.

• 30 Days Past Due: The servicer sends a breach letter or Notice of Default, formally notifying the borrower of the delinquency and the lender’s right to accelerate the loan.

• Notice of Sale Published: Under Georgia law (O.C.G.A. § 44-14-162), the lender must advertise the foreclosure sale in a local newspaper in the county where the property is located, once a week for four consecutive weeks before the sale date.

• Foreclosure Sale Date: The sale takes place on the first Tuesday of the month at the county courthouse. In Fulton County, this is the Fulton County Courthouse in downtown Atlanta. The property is sold to the highest bidder. The process is public, final, and irreversible.

From Notice of Sale publication to the auction: as few as 37 days. From the first missed payment to auction: potentially 60 to 90 days total. For context, California’s non-judicial process requires a minimum of 111 days. Florida’s judicial process routinely takes 6 to 12 months. Georgia is among the fastest foreclosure states in the country, and Fulton County homeowners face that reality directly.

There is another critical difference from tax sales: Georgia’s non-judicial foreclosure process provides no statutory right of redemption after the sale. Once the courthouse steps sale is complete and the foreclosure deed is issued to the winning bidder, the former homeowner loses all legal rights to the property immediately. There is no 12-month window to reclaim it. There is no buyback option. The sale is final.

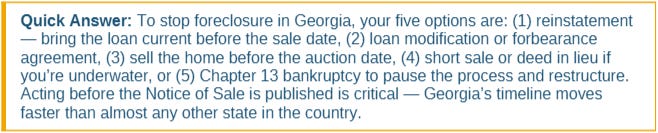

The critical window: Once the Notice of Sale is published in the newspaper, you have weeks — not months — to act. Every strategy in this guide must be initiated before the auction date. After the courthouse steps, none of these options exist.

Option 1 — Reinstatement: Bring the Loan Current Before the Sale Date

Reinstatement is the cleanest and most complete solution available to a Georgia homeowner facing foreclosure. It means paying everything past due — in a single lump sum — to bring the mortgage completely current and stop the foreclosure process in its tracks.

What the Reinstatement Amount Includes

The reinstatement figure is not simply your missed monthly payments. It includes every cost the lender has incurred in the process of pursuing foreclosure against you. Expect the payoff to include all missed principal and interest payments, late fees for each delinquent month, property inspection fees the servicer conducted, attorney fees incurred by the lender during the foreclosure process, the cost of the newspaper foreclosure advertisement, and any forced-placed insurance premiums if your homeowner’s insurance lapsed.

The total is almost always higher than homeowners expect — and it changes monthly. Get a written reinstatement quote with an expiration date directly from your servicer’s loss mitigation department, not the general customer service line.

Georgia’s Reinstatement Right

Under Georgia law, borrowers have the right to reinstate the loan up until five business days before the scheduled foreclosure sale date. This is a hard deadline — reinstatement must be paid in certified funds (cashier’s check or wire transfer). Personal checks are not accepted and will not stop the sale.

Reinstatement is the best option when it is financially accessible because it preserves the original loan terms, stops the foreclosure completely, and allows the homeowner to remain in the property without any change to the mortgage. If the full reinstatement amount is out of reach, the next options provide alternatives.

If the reinstatement amount is close but you need a short window to gather funds, ask the servicer’s loss mitigation department specifically about a short-term forbearance that runs alongside a reinstatement agreement. Some servicers will accommodate this — but you must ask directly and get it in writing.

Option 2 — Loan Modification and Forbearance Agreements

For homeowners who want to keep their home but cannot come up with the full reinstatement amount, a loan modification or forbearance agreement may provide a structured path to stay in the property — without requiring a lump sum payment.

Loan Modification

A loan modification is a permanent change to the original terms of your mortgage — the interest rate, the loan term, the monthly payment amount, or in some cases the principal balance — that brings the payment to a level the homeowner can sustain going forward. Modified terms are negotiated with the servicer and formalized in a written agreement. Once approved, the homeowner resumes making the modified payment and the foreclosure process is suspended.

Forbearance

A forbearance agreement is a temporary reduction or pause in mortgage payments, typically lasting three to six months, after which the homeowner repays the paused amount through a structured repayment plan, a lump sum, or through deferral to the end of the loan. Forbearance does not erase what was missed — it restructures when and how it is repaid.

The Application Process

Both options require submitting a complete loss mitigation application to the servicer’s loss mitigation department. A complete application typically includes a signed hardship letter explaining the circumstances that led to the default, the two most recent pay stubs, the two most recent bank statements, the two most recent federal tax returns, and a completed financial worksheet showing monthly income and expenses.

Under the Consumer Financial Protection Bureau’s mortgage servicing rules, a servicer cannot proceed to a foreclosure sale while a complete loss mitigation application is under review. This is called the dual-track prohibition, and it is one of the most important legal protections available to Georgia homeowners. Filing a complete application — not a partial one — triggers this protection. The CFPB mortgage servicing rules that protect homeowners from dual tracking are federal regulations that apply to all servicers regardless of the state.

The Role of a HUD-Approved Housing Counselor

Free HUD-approved housing counselors can help prepare a complete loss mitigation application, communicate with the servicer on the homeowner’s behalf, and advocate for a fair evaluation. Research consistently shows that homeowners who work with a counselor have significantly better outcomes than those who navigate the process alone. This service is free and available across Metro Atlanta.

Option 3 — Sell the Home Before the Foreclosure Sale Date

This is the option most Atlanta homeowners overlook until the window is almost closed — and in today’s Fulton County market, it may be the most financially powerful tool available to a homeowner facing foreclosure.

The core insight is this: if your home is worth more than you owe on it, a foreclosure is not just a threat to your housing — it is a threat to your wealth. Allowing a lender to foreclose on a home with equity means surrendering that equity to the foreclosure process. The courthouse steps sale generates nothing for the homeowner. A voluntary sale before that date captures the equity and puts it in the homeowner’s pocket.

Traditional Sale

If there is enough time on the foreclosure clock and the home is in sellable condition, a traditional listing with a real estate agent can generate full market-rate proceeds. In Atlanta’s current market, this is a legitimate option for homeowners who are early in the foreclosure timeline. The average time from listing to closing in Atlanta is 30 to 60 days — which works if the Notice of Sale has not yet been published, but becomes a tight race against the clock once it has.

As-Is Cash Sale

For homeowners facing an imminent foreclosure date, an as-is cash sale to a real estate investor or cash home buyer can close in 7 to 21 days. No repairs required. No showings or staging. No agent commissions. At closing, the outstanding mortgage balance, any delinquent property taxes, HOA arrears, and other liens are paid directly from the proceeds. The homeowner walks away with whatever equity remains.

The math is straightforward: a Fulton County home worth $300,000 with a $210,000 mortgage balance and $15,000 in missed payments and fees still represents $75,000 in equity. A cash sale at $270,000 recovers most of that. A courthouse steps auction recovers none of it. Understanding Georgia homeowner rights during the foreclosure process — including the right to sell at any point before the sale date — is essential knowledge for every homeowner in this situation.

Addressing the Emotional Barrier

Many homeowners in foreclosure delay acting because of embarrassment or the hope that something will work out on its own. In Georgia, that delay has a direct financial cost. A home in foreclosure in 2026 Fulton County likely has equity. Acting before the auction preserves it. Waiting until after the auction means that equity is gone. This is a financial decision, not a moral judgment — and framing it that way is often what allows homeowners to act in time.

Option 4 — Short Sale or Deed in Lieu for Underwater Homeowners

Not every homeowner facing foreclosure has equity. For those whose mortgage balance genuinely exceeds the property value — who are truly underwater — a traditional or cash sale may not generate enough proceeds to pay off the loan. In this situation, two additional exit strategies are available: the short sale and the deed in lieu of foreclosure.

Short Sale

In a short sale, you sell the home for less than the outstanding mortgage balance with the lender’s prior approval, and the lender agrees to accept the sale proceeds as full or partial satisfaction of the debt. The sale stops the foreclosure and allows the homeowner to exit the property without a completed foreclosure on their record.

The most important element of any short sale negotiation is the deficiency waiver — the lender’s written agreement to not pursue the remaining balance after the sale. This must be explicitly negotiated and confirmed in writing before the closing. Never assume a short sale eliminates the deficiency without seeing it in the lender’s written approval letter. A short sale typically takes three to six months from start to close, which means it requires an early start relative to Georgia’s fast foreclosure clock.

Deed in Lieu of Foreclosure

In a deed in lieu, you voluntarily transfer the property title directly to the lender in exchange for a release from the mortgage obligation. There is no sale, no listing, no buyer — just a direct title transfer. The lender typically requires that no other liens exist on the property (no second mortgage, no HOA lien, no IRS tax lien), that the property has been listed for sale unsuccessfully for a minimum period, and that the borrower can demonstrate genuine hardship. The process typically takes 30 to 90 days and sometimes includes relocation assistance from the lender.

Tax Consequences of Both Options

Both a short sale and a deed in lieu can trigger cancellation of debt income — the IRS may treat the forgiven deficiency balance as taxable income in the year the transaction closes, resulting in a 1099-C from the lender the following January. The Mortgage Forgiveness Debt Relief Act and the insolvency exemption under IRS Form 982 may significantly reduce or eliminate this tax event for qualifying homeowners. Consult a tax professional before closing either transaction — not after.

Option 5 — Bankruptcy as a Temporary Foreclosure Pause

Bankruptcy is a federal legal tool that, in the right circumstances, can stop a Georgia foreclosure sale immediately — even on the morning of the auction. It is not the right option for everyone, and it carries significant long-term credit consequences. But for homeowners who have a path to keeping their home and need time to execute a plan, it deserves serious consideration.

How Bankruptcy Stops Foreclosure

Filing any bankruptcy petition triggers an automatic stay under federal bankruptcy law. The automatic stay is an immediate, court-ordered halt to all collection actions against the borrower — including a scheduled foreclosure sale. The moment the bankruptcy petition is filed with the court, the foreclosure sale is legally prohibited from proceeding. Lenders can file a motion to lift the stay, but this process takes time, providing the homeowner a window to negotiate.

Chapter 13: The Option for Homeowners Who Want to Keep the Home

Chapter 13 bankruptcy allows homeowners to restructure their debt and catch up on missed mortgage payments through a court-approved repayment plan lasting three to five years. During the plan, the homeowner makes two sets of payments: the current regular mortgage payment directly to the servicer, plus a portion of the arrears through the plan payment to the bankruptcy trustee. If all plan payments are made over the three to five year period, the mortgage is brought fully current and the homeowner keeps the home.

Chapter 13 requires regular income sufficient to fund both the plan payment and the ongoing mortgage. It is not available to homeowners with no income, and it is a serious multi-year commitment. Failure to maintain plan payments results in dismissal of the case and resumption of the foreclosure. Consult a Georgia-licensed bankruptcy attorney to determine whether your income and debt profile make Chapter 13 viable.

Chapter 7: Buying Time, Not Keeping the Home

Chapter 7 bankruptcy discharges unsecured debt but does not permanently stop a mortgage foreclosure. The automatic stay is temporary — the lender can file a motion to lift the stay, and the foreclosure typically resumes within 60 to 90 days. Chapter 7 is most appropriate when the homeowner intends to eventually exit the property but needs additional time to relocate, prepare financially, or coordinate a transition. For a full explanation of how the federal automatic stay works, the federal bankruptcy basics and the automatic stay explained resource from the U.S. Courts provides authoritative, plain-language guidance.

Important: Bankruptcy requires a Georgia-licensed attorney. Serial filings result in shorter automatic stay periods. The credit impact lasts 7 to 10 years. Do not file without professional legal counsel who can assess whether Chapter 13 or Chapter 7 is appropriate for your specific situation.

The Fastest Path Forward — Choosing the Right Option for Your Situation

Every option in this guide is available to you right now. None of them will be available after the courthouse steps sale. Here is how to match your situation to the right strategy.

If you have the funds to catch up: Call your servicer’s loss mitigation department today and request a written reinstatement quote with an expiration date. Pay it in certified funds before the five-business-day cutoff. This is the cleanest path — it stops the foreclosure completely and preserves your original loan terms.

If you need to keep the home but can’t pay the lump sum: Submit a complete loss mitigation application for a loan modification or forbearance immediately. A complete application — not a partial one — triggers the CFPB’s dual-track prohibition and legally prevents the servicer from proceeding to sale while it is under review. Get a HUD counselor to help you prepare it.

If you have equity and need to exit: Sell before the auction date. This is the wealth-preserving option. If the Notice of Sale has not yet been published, a traditional listing may work. If the clock is tight, an as-is cash sale that closes in 7 to 21 days is the right tool. Every day of delay is a day of equity at risk.

If you’re underwater and cannot pay the shortfall: Negotiate a short sale or deed in lieu with your lender. Start as early in the process as possible — both require lender cooperation and both take time. Confirm the deficiency waiver in writing and consult a tax professional before closing.

If you need to buy time and have income to fund a plan: Consult a Georgia-licensed bankruptcy attorney about Chapter 13. Understand that it is a 3 to 5-year commitment with strict payment requirements — but for homeowners with regular income who genuinely want to keep their home, it is a legally available and sometimes the right path.

The single most important message of this entire guide: every one of these options requires you to act before the foreclosure sale date. After the courthouse steps, the property belongs to the winning bidder and none of these strategies can help you. The homeowners who protect their homes and their equity are the ones who make a phone call today — not next week.

Connect with a free HUD-approved foreclosure counselor in Atlanta, Georgia to get a professional assessment of your specific situation at no cost. These counselors are trained specifically to help homeowners navigate exactly the kind of situation described in this guide.

Final Thoughts: In Georgia, Time Is the One Thing You Cannot Get Back

Georgia’s foreclosure system is fast, final, and unforgiving. But it is not hopeless — as long as you act before the auction. Reinstatement, modification, a pre-sale, a short sale, a deed in lieu, a bankruptcy filing — these are real options with real outcomes that thousands of Georgia homeowners use every year to protect their homes and their equity.

What separates the homeowners who come out ahead from those who lose everything at the courthouse steps is almost always one thing: acting early enough to still have a choice. If you’re reading this, you still have time. Use it.

Facing Foreclosure in Fulton County or Metro Atlanta? Don’t Wait.

If you’re facing foreclosure in Fulton County or anywhere in Metro Atlanta, don’t wait until the courthouse steps to make a decision. I’m Gerald Harris, founder of Atlanta Housing 411, and I work with homeowners across Atlanta who are navigating foreclosure, tax delinquency, and difficult housing situations every day. Whether you need to understand your timeline, figure out whether you have equity worth protecting, or simply know which phone call to make first — I can help you think it through without pressure and without judgment.

In Georgia, time is the one thing you cannot get back once the gavel falls.

📞 Call or Text: 404-913-7086 📧 Email: atlanta285.com@gmail.com

Visit Atlanta Housing 411 — Contact Gerald Harris — No pressure